Key Takeaways

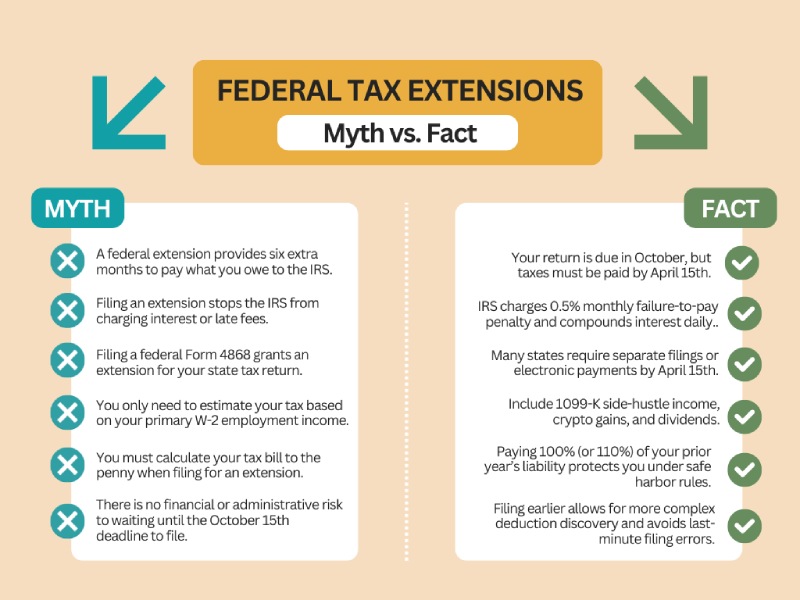

- A federal extension provides six extra months to file, but all taxes owed must still be paid by the April 15th deadline to avoid penalties and interest.

- For 2026, the IRS assesses a 0.5% monthly failure-to-pay penalty plus 7% annual interest (compounded daily) on any balance remaining after April 15.

- To prevent underpayment penalties, ensure your April payment covers at least 90% of your 2026 liability or 100% of your prior year’s total tax (110% if your AGI exceeded over $150,000).

- Your federal extension (Form 4868) may not cover your state return. Many states require separate filings or specific electronic payments by the April deadline to grant an extension.

- Extension estimates often fail because taxpayers overlook taxable events like 1099-K side-hustle income, crypto/stock capital gains, or high-interest savings account dividends that lack standard withholding.

Filing for a federal tax extension isn’t just a pause button on your tax obligations.

It’s a bridge to your final return that needs to be crossed strategically.

And if you treat a tax extension as a way to simply push taxes out of your mind until October, you could end up facing some pretty heavy penalties.

So, to help you use this extra time to your advantage, I’ve outlined the six mistakes I most often see Orange County taxpayers make, and steps you can take to stay compliant.

Mistake #1: Thinking an extension gives you more time to pay

Yes, your return is on extension, but your unpaid tax balance is still due on April 15th. And your balance is exposed to penalties and interest if you miss that deadline.

If you file an extension but fail to pay the full balance due, you’ll be assessed a failure-to-pay penalty of 0.5% of the unpaid amount for each month (or partial month) that tax remains unpaid. Which can accrue up to a max of 25%.

On top of that, the IRS charges underpayment interest that compounds daily on the remaining balance. For 2026, the rate is 7% annually, compounded daily.

The extension does protect you from the much harsher 5% monthly failure-to-file penalty. But the combination of the 0.5% penalty and daily interest means your most effective strategy is to pay as much of your estimated balance as possible by the April deadline.

Mistake #2: Not making a partial payment

Even if you can’t pay your balance in full by April 15th, a partial payment can do three useful things:

1. Reduce the unpaid amount subject to ongoing penalties and interest

Every dollar you can pay by the April 15th deadline reduces the amount the IRS uses to calculate your penalties and interest. Since the failure-to-pay penalty and daily compounded interest are percentage-based, lowering the base balance directly shrinks the rate at which your debt grows.

2. Show that you made a good-faith effort to address the liability

Making a partial payment demonstrates good faith on your part. It shows your intent to comply, which can go a long way when requesting a payment plan or penalty abatement later.

Plus, if you file on time and set up an approved payment plan, the failure to pay rate is typically halved to 0.25% per month.

3. Make the eventual bill payment less painful

Think of it like stopping a leak. You might not be able to fix the pipe entirely right now, but reducing the flow prevents your tax bill from ballooning into a much more unmanageable figure over the coming months.

Mistake #3: Failing to make a reasonable tax estimate

The IRS only grants a penalty-free extension if your payment covers at least 90% of your total tax liability by the April deadline. If your estimate is too low and you underpay beyond that threshold, the failure-to-pay penalty is applied retroactively to the entire unpaid balance from April 15th.

How to calculate your estimated tax liability

To arrive at a reliable figure without having completed your full return, follow these steps:

1. Collect all forms of income earned throughout the year, including:

- W-2s from employers.

- 1099-NEC/MISC for freelance or contract work.

- 1099-INT/DIV for interest and dividends.

- Realized capital gains from stock or crypto sales.

2. Apply the safe harbor rule. This means paying:

- 90% of the current year’s tax liability, or

- 100% of the total tax shown on your prior year’s return (110% of the prior year’s tax if your Adjusted Gross Income (AGI) was over $150,000).

3. Use a tax estimator tool.

The IRS Tax Withholding Estimator is best if you’re a W-2 employee. And if you’re self-employed, a self-employed tax calculator can help you factor in the 15.3% self-employment tax on top of income tax.

4. Account for deductions and credits.

Subtract above-the-line deductions (such as Student Loan Interest or HSA contributions) to find your Adjusted Gross Income. Then, subtract either the standard deduction or your estimated itemized deductions to find your taxable income.

(There are a lot of factors to balance here, I know. So, if you’d rather someone who does this for a living take the time to figure it out for you, my door is open: calendly.com/tom-ameritax/new-meeting).

Mistake #4: Overlooking hidden taxable events

Most Costa Mesa taxpayers focus on the numbers on their final W-2 of the year. But overlooking off-paycheck taxable events is a big way to trigger a failure-to-pay penalty.

To make sure your extension payment is accurate, you need to look beyond your primary employer and audit your financial year for these commonly missed events:

1. Capital gains and digital assets

Selling stocks, bonds, or cryptocurrency can create a massive tax spike. For the 2026 tax year, the IRS has expanded reporting requirements for digital assets, meaning these transactions are more visible than ever. Even if you haven’t received the paperwork, you must estimate the gains to avoid an underpayment surprise.

2. Side-hustles and gig work (1099-K & 1099-NEC)

Income from platforms like Uber, Etsy, or freelance consulting often has zero tax withholding. You are responsible for both income tax and the 15.3% self-employment tax. (Forgetting this shadow tax is the number one reason extension estimates fall short.)

3. Interest and dividends (1099-INT & 1099-DIV)

High-yield savings accounts and brokerage dividends might seem small, but in a high-interest rate environment, they can add thousands to your taxable income.

4. Retirement account activity

If you took an early withdrawal from a 401(k) or converted a Traditional IRA to a Roth IRA, you’ve created a taxable event. These actions often carry heavy tax weights that aren’t reflected in your monthly paychecks.

Again, I always tell my Orange County clients to rely on the safe harbor rule here: By paying 100% (or 110%) of what you owed last year, the IRS generally waives the underpayment penalty even if your actual bill for this year ends up being much higher.

Mistake #5: Assuming your state return follows your federal extension automatically

A common and costly mistake I see among taxpayers is assuming that filing a federal tax extension automatically covers their state obligations. In reality, tax laws vary significantly by state. And assuming uniformity can lead to failure-to-file penalties at the state level.

Some states do grant an automatic extension if you have a valid federal one. But others require a separate state-specific filing or a state-level payment by the original deadline to keep the extension valid.

If your state is one that requires a separate action and you miss it, you could face state penalties (that are often more aggressive than federal rates).

How do state tax extensions work?

There are three distinct categories of state extension rules. And knowing which category your state falls into is the only way to avoid surprise notices.

1. States with automatic extensions.

Some states (like California or Wisconsin) grant an automatic extension to all residents regardless of whether a federal extension was filed. But you must still estimate and pay your state liability by April 15th.

2. States that mirror federal extensions.

States like New York generally recognize your federal extension, but only if you have no balance due. If you expect to owe state taxes, many of these states require you to file a specific state form and submit your payment simultaneously to avoid late-filing status.

3. States requiring separate filings.

States like Pennsylvania or Tennessee require their own unique forms. If you rely solely on your federal Form 4868, these states will consider your return late the moment the April deadline passes.

How to protect your state filing status when filing a tax extension

To ensure you aren’t blindsided by state-level penalties, follow this three-step verification process:

- Check the payment-vests-extension rule: Many states consider your extension automatically granted only if you pay 100% of the estimated tax due via the state’s online portal by the deadline. No payment often means no extension.

- Verify form requirements: Visit your state’s Department of Revenue website to see if they require a copy of your Federal Form 4868 to be attached to your eventual state return.

- Don’t forget no-income-tax states: Even if you live in a state with no earned income tax (like Florida or Texas), you may still have state-level filing requirements for business entities or tangible personal property that do not follow federal timelines.

Mistake #6: Waiting until October to file

While a federal extension buys you until October 15th to submit your paperwork, waiting until the final hour is a high-risk strategy that can lead to compounding financial and administrative headaches. Filing too close to the October deadline creates several disadvantages:

- If you made a math error in your April estimate, waiting until October to file means you’re still accruing daily interest on that small discrepancy.

- If you plan on applying for a mortgage, a student loan (FAFSA), or a business line of credit, lenders typically require your most recently filed tax return as proof of income.

- If a life emergency, technical glitch, or missing document prevents you from filing by October 15th, you move immediately into failure to file territory. This triggers the penalty of 5% per month of the unpaid tax.

- As your tax pro, I can tell you: I’ll be overbooked during the first two weeks of October. If you wait until then to hand over your records, you might have to pay higher rush fees.

And beyond just avoiding risks, filing early could help you maximize your tax savings. Because you get to secure my full attention as your tax pro during the least stressful months of my year.

This could benefit you in three key ways:

- By filing earlier, your preparer has the time to thoroughly dig for complex deductions (like home office expenses, energy-efficient home improvements, or complex business travel) that could apply to your situation.

- Filing early allows us to identify any missing records, giving you weeks to track down the documentation needed to legally claim a credit or deduction.

- When you finish your taxes early, we can pivot to tax planning strategies while you still have half the year left to take action.

Final thoughts

Filing for a federal tax extension is a strategy for accuracy and control. Not a way to push your return out of your mind even longer.

Your estimate matters, your payment matters, your state filing matters, and your follow-through definitely matters.

But you don’t have to figure all of that out solo. Grab a time to talk to me, and I can help you wherever you’re at: whether you’re not sure how much to pay, you know you can’t afford your balance, or you just want to get filed early so you can secure the most savings.

calendly.com/tom-ameritax/new-meeting

FAQs

“How can I confirm the IRS received my tax extension?”

If you filed electronically, you should receive a confirmation email from your software provider or a Submission ID within 24–48 hours. If you are unsure, the most reliable method is to log in to your IRS Online Account at IRS.gov. Once logged in, check your tax records or transcript to see if Form 4868 has been processed.

“Can I get an extension without filing Form 4868?”

Yes. If you make a full or partial tax payment electronically using IRS Direct Pay, the Electronic Federal Tax Payment System, or a debit/credit card, you can select “Extension” as the reason for payment. The IRS will automatically grant you an extension to file without requiring a separate Form 4868.

“What should I do if my tax extension is denied?”

Extension denials are rare and usually caused by a typo in your Social Security Number or a name mismatch. If the IRS rejects your extension, you generally have a five-day grace period from the date of the rejection to correct the errors and resubmit it. If you miss this window, you must file your full return as soon as possible to minimize late-filing penalties.

“If I overpaid my extension estimate, how do I get my refund?”

You’ll claim the amount you paid with your extension as a payment on your final tax return. If that payment, combined with your withholdings, exceeds your actual tax liability, the IRS will issue the excess as a refund or allow you to apply it toward next year’s estimated taxes.

“Can I get tax penalties removed if I missed the April deadline?”

Yes, you may qualify for the IRS First-Time Abate (FTA) program. If you have a clean compliance history for the past three years (meaning no penalties) and have filed all currently required returns, you can request a one-time administrative waiver of the failure-to-file and failure-to-pay penalties.

“I live in a disaster area. Do I still need to file an extension?”

If the IRS has declared a federal disaster area for your location, you’ll receive an automatic extension to file and pay without filing for a federal tax extension using Form 4868. But you should always check the Tax Relief in Disaster Situations page on the IRS website to see if your specific county and the 2026 deadlines have been officially postponed.